The article has been republished with permission of the authors Chewe Mwila, Gerald Soko, Patrick Chileshe economists with Zanaco Bank

… What it Seeks to Achieve

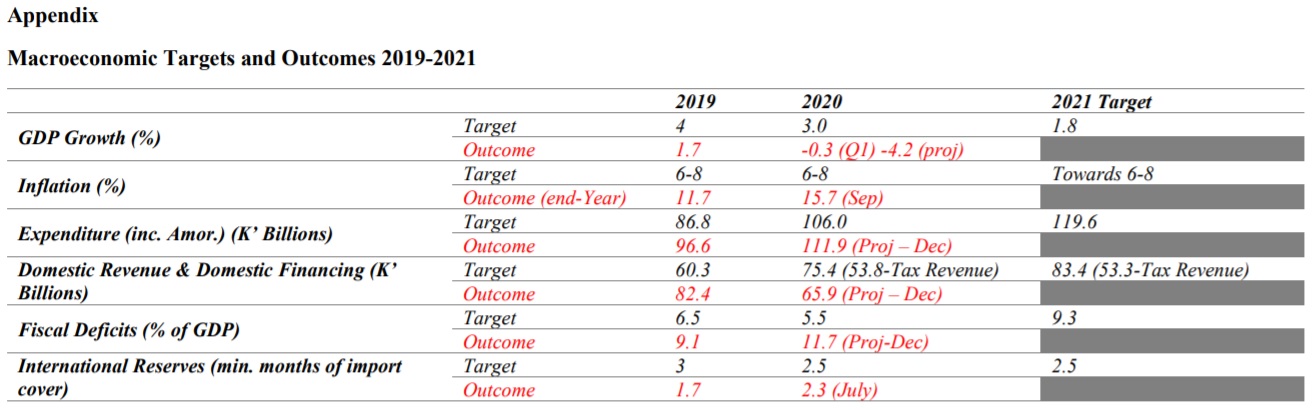

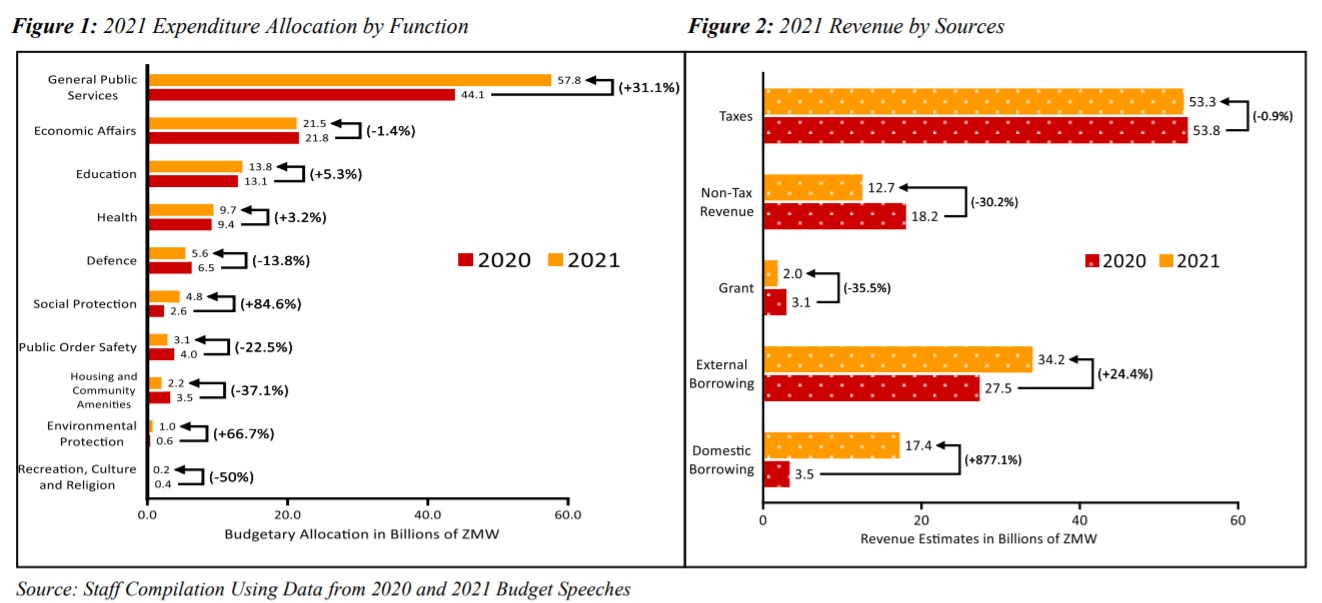

Zambia plans to spend a total of ZMW 119.60 billion for the 2021 fiscal year, up 12.8% from ZMW 106 billion for 2020. Minister of Finance, Dr. Bwalya Ngandu, unveiled this during the 2021 budget presentation themed “Stimulate Economic Recovery and Build Resilience to Safeguard Livelihoods and Protect the Vulnerable.” In all this, Africa’s second-largest copper producer aimed to achieve a minimum of 1.8% in real GDP growth, reduce inflation towards the 6-8% central bank target range, increase gross international reserves to 2.5 months of import cover, narrow the fiscal deficit to 9.3% of GDP as well as achieving domestic revenue collections of not less than 18% of GDP. Expenditure allocations by a function of government are given in Figure 1 while Figure 2 presents the sources of finances/revenue

… The Meat of the Budget

… The Meat of the Budget

Coming from a year that has caused so much economic pain globally and domestically, the budget objectives paint a picture of an economy that is headed for slight recovery while attempting to ensure macroeconomic stability. Key positives that stand in partial support of the budget targets are the removal of the import duty on copper ores and concentrate (good for the mining sector); a 20-percentage-point reduction in the corporate income tax for hotels and lodges on accommodation and food services to 15% (has come at a good time for tourism players); the upward shift in the PAYE tax bands by ZMW 700 (low earning employees are the real gainers); suspension of import duty on refrigerated trucks; and zero-rating of VAT on tractors (a smile for commercial farmers). Farmers operating in the horticulture and floriculture space also walked away with a range of perks. Also, the increased allocation on social protection seems to sit well with safeguarding livelihoods and protecting the vulnerable.

… Is the 2021 Expenditure a Contracting Expansion?

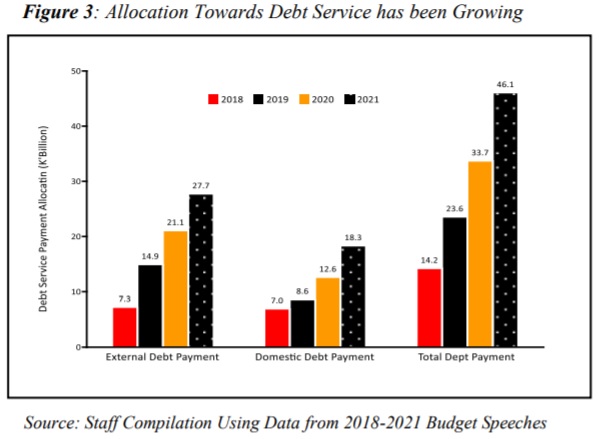

Although the budget size was up 12.8% compared to this year’s, the increase was not a fresh injection of cash to stimulate the economy but was mainly due to the increase in debt service obligations under the general public service function. In particular, the general services function was up 31.1% to ZMW 57.8 bn (48.3%) with over 84% going to debt service. Moreover, the increase in the total budget amount (ZMW 13.6 billion) is wholly swallowed by an increase in allocations towards debt service obligations (have gone up ZMW 13.7 million). On the other hand, resources for most important economic affairs functions were cut down 1.4% to ZMW 21.5 bn after allocations on roads, international airports and strategic food reserves took knocks of 41.1%, 68.9%, and 21.6% respectively because of allocations to election activities and MPs gratuity. Meanwhile, increased budgetary allocation to education, health, social and environment protection wholly (changes sum almost to zero) come at the back of reductions on defense, housing and community amenities, public order safety, and recreation/culture/religion. Put together, the expenditure side shows that the increased 2021 budget size will feed the monster in ballooning debt while starving economic affairs.

… The Making of Revenue Estimates and the Domestic Credit Market Raid

… The Making of Revenue Estimates and the Domestic Credit Market Raid

When the government intended to grow this year’s size of the economy by 3%, they projected that such a growth rate would generate ZMW 53.8 billion in taxes. With the COVID-19 shock, BoZ’s projections indicate that the economy will shrink by more than 4% and if the economy grows by 2.5% (most likely outcome as forecasts from many), then the size of the economy in 2021 will be small than 2019 one. Given the foregoing, we highly doubt that we can hit the tax revenue target (little changed from the figure we hoped to achieve with an economy 3% bigger than 2019’s) with a smaller economy. Besides, a significant proportion of firms will still be nursing the 2020 wounds while we also do not expect a full absorption of all workers that lost their jobs this year (firms were reducing staffing levels in August for the seventh month in a row). In such an economy, we find it hard to think of where the 15.3% and 4.3% increases in company income tax and personal income tax will come from.

Concerning other sources, we have duly recognized that there will be difficulties in the collection of revenues from non-tax sources, grants, and as well as from external creditors. As regards external debt, the other good news is that very few commercial creditors can offer us funds given our current external debt issues and so we expect that the ZMW 34.2 billion will largely come from concessional lenders. The biggest worry in our next year’s financing strategy is the intention to raid the domestic credit market, which already has a bias of lending to the government at the expense of the private sector. The ZMW 17.4 billion (equivalent to 14.6% of the total budget) we intend to borrow from domestic lenders will surely continue disadvantaging the productive private sector and therefore puts into question the feasibility of the growth target. Also, the government has only allocated ZMW 2.8 billion towards the dismantling of arrears that are sitting well above ZMW 20 billion owed to a private sector that has been lamenting the lack of liquidity in the economy.

… The Road to Debt Sustainability

The appointment of the Lazard Freres of France to reorganize the country’s external debt portfolio earlier this year stands out as the key debt management strategy and possibly a key milestone already in getting Zambia’s debt position to a sustainable path. The budget also touched on the cancellation of some pipeline loans (US$ 1.1 billion) and re-scoping of some of the projects (downgrade of some roadworks from bituminous standard to gravel fit here). However, the heavy reliance on the domestic credit market for financing of government activities is beginning to worry and maybe undoing efforts on the external front. The budget does indicate that government intends to ‘alter the domestic debt portfolio from shorter to longer-term instruments’ but the truth is that it has no control over this because it depends on investors that have for long preferred treasury bills over bonds. Even under the assumption that the foregoing is achieved, it only results in back-loading the country’s liabilities and therefore compromised sustainability of the intended recovery. All in all, the debt management strategy is unlikely to ensure the country returns to debt sustainability soon. Moreover, the 9.3% fiscal deficit does not sit well in a debt sustainability story.