Managing Director Owen Silavwe, commented

I am pleased that the 2022 results have highlighted continued improvement in the Group’s overall performance. The Group is in a much better position today to focus on its strategic priorities and deliver long-term economic benefits to its stakeholders in the regions where we operate. As we witness continuing improvements in the business environment coupled with government efforts to create a private sector-led economy effective and efficient execution of our strategy should deliver steady growth of the business over the coming years.

We continue to deliver on our operational and financial performance. We managed our network efficiently, ensuring safe and reliable delivery of energy to our customers . Financial performance remains very strong . We made good progress on our strategy as we began to roll out key power infrastructure projects that will strengthen our power supply portfolio, enhance our role in the transition to a cleaner energy future and enable us to move more power to places where it is required by our customers to meet their growing demand. We achieved good progress in addressing key historical issues faced by the business that we have reported on in previous periods. In this regard, I am happy to report that we resolved almost all the historical issues with the exception of one. The first being the signing of a new Bulk SupplyAgreement (BSA) with ZESCO, effective April 2022 with a tenure of 13 years. Secondly, we signed a settlement agreement with ZESCO covering the terms to apply for the gap period of 1 April 2020 to 31 March 2022. The wto agreements have effectively eliminated the uncertainty in respect of applicable commercial terms in the provision of services between the two entities. This has also settledany contingent asset or liability that may have been associated with the gapperiod. Working with the mines, the Energy Regulation Board(“ERB”)and ZESCO, we reached a Consent Judgement reversing the ERB’s tariff increase to the mines of 2014.The Consent Judgement has effectively extinguished the contingent asset and liability of USD227.0 million on the sale and purchase sides respectively that the Group had reported in last year’s results. Notwithstanding the headway made in addressing the historical issues, the Konkola CopperMines Pel debt remains unresolved. The arbitral proceedings relating to this matter, which commenced in 2021,are ongoing.

Balancing how we manage our assets to deliver, over the long-term, safe, reliable, and affordable energy for our customers based on long-term contracts in an evolving regulatory environment, alongside the inescapable need to embed an effective risk management framework to continuously minimise business risk si key to the delivery of value to our stakeholders.We are continuing to invest ni our power network, achieving asset upgrades and modernisation, which enable more efficient and reliable service delivery to our customers.

The total energy demanded by our customers and transmitted through our network totalled 5,913GWh, a growth rate of over 3% compared to 5,717GWh recorded in 2021. This covers power demand across al business segments- local power

supply, domestic and international wheeling, transmission use of system and regional power supply. We expect the upward trend in demand to continue in the medium to long-term, driven primarily by anticipated mining activity ramp up both in the Zambian and DRC markets. The long-term value creation is underpinned by growth opportunities we se in both markets that should drive financial performance. During the year, we signed supply contracts with a number of new customers with aprojected total demand of about 80MW. Scale up in demand is expected to happen over a two-year period.

We commissioned new infrastructure connecting two of the customers, namely Macrolink and Mimbula mines. The construction of power assets to connect Lonshi mine to the network is underway, with commissioning expected in 2023.

We look ahead with optimism as we see great growth prospects based on increasing economic activity in the regions where we operate, disciplined strategy execution and the positioning of our business done over the last two years to work more collaboratively with our key partners. During the year, we evolved our strategy to repurpose and refocus the business to capture opportunities that best align with our core business and put operational excellence at the heart of how we create value and efficiently meet their requirements. This will see us invest more than US$200 million over the next 3years in new transmission and distribution infrastructure and energy transition initiative to support both organic and new business growth. As demand for power ramps up, we need to strengthen our supply portfolio from which this demand wil be reliably and affordably supplied. To corroborate our buoyancy, we are working hard to deliver on a pipeline of projects that will ensure that we consistently deliver on our operational and financial performance targets. We operate in an industry where the pace ofchange si accelerating with increased focus on decarbonisation, digitalisation, anddecentralisation. Our strategy is increasingly being adapted to reflect these changes. As part of our renewables strategy, our flagship solar projects are at different stages of implementation. The 34MW Riverside solar project was officially commissioned post balance sheet on 15 February 2023 by the President of the Republic of Zambia, M.r Hakainde Hichilema. The 60MW Garneton solar project si under construction and is planned to be commissioned in December 2023. Renewable projects are being implemented through CEC Renewables, a 100% subsidiary of CEC. We are working with our partners with the aim of adding significant Interconnector transmission capacity to facilitate further growth for the power trading business segment which has seen annual average growth rates of over 8%. The planned first phase for this workstream is currently under implementation with the aim of increasing the Interconnector capacity between Zambia and DRC to 400MW from 230MW by end of 2024. As we pursue these growth opportunities, we aim to maintain a disciplined approach to our investments, manage our financial risks and ensure consistent and progressive dividend delivery to our shareholders.

Financial Highlights

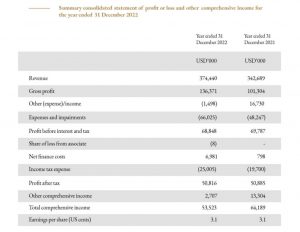

Group revenue increased by9 toUSD374.4 million (2021: USD342.7 million)driven mainly by higher local power sales, wheeling sales and regional power sales of9%, 45% and 12% respectively. Profitability remained fat at USD50.8 million (2021: USD50.9million) onthe back of higher impairment loss of USD24.1 million (2021: USD12.6 million), driven by the recalibration of the I R S 9impairment model. Cash costs increased to USD41.9 million (2021: USD35.6 million) owing to the Kwacha appreciating yb 15% on average. The exchange rate averaged ZMW16.93:USD1 in 2022 (2021: ZMW19.96).

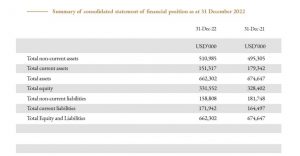

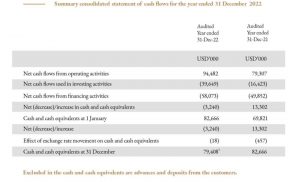

The general improvement in collections positively impacted the liquidity position, resulting in cash flow from operations of USD94.5 million (2021: USD79.3 million) and a cash balance of USD83.4 million (2021: USD92.7 million).

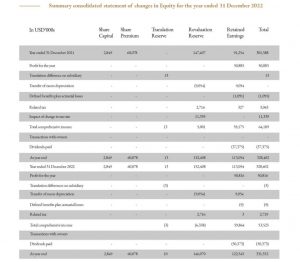

The Group, having addressed some of the key uncertainties it had faced and backed by both the dividend policy and the strength of the financial performance, declared and paid an interim dividend of USD50.4 million, which represents a 35% increase over the 2021 dividend distribution

ofUSD37.4 million.The entity results are included in the 2022 Annual Report.

Cautionary on forward looking information

This summary results announcement contains financial and non-financial forward-looking statements about the Company’s performance and position. We believe that while all forward-looking information contained herein is realistic at the time of publishing this report, actual results in future may differ from those anticipated. These forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause CEC’s actual results, performance or achievements ot differ materially from the anticipated results, performance or achievements expressed or implied by these forward-looking statements. Although CEC believes that the expectations reflected in these forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have ben correct. We take no obligation to revise or update these forward-looking statements to reflect events or circumstances that arise after the statements have been made.

{kind=link}