FNB Zambia releases monthly reports which illuminate key factors affecting players within the agriculture sector. The report monitors the price movements of three key commodities: maize (+45%) , soya (+59%) and wheat (+29%). Over the course of the last year there have been significant price increases to commodities as a result of the global supply chain instability caused by Russia’s invasion of Ukraine. Soya and Wheat are the crops with the most international exposure and farmers are expected to benefit from the international speculation. The general food price indexes showed an overall increase of an average +8% in the price of key consumer foods. In this article we break down some of the key market analysis within the contents of the report.

Key Commodity Price Highlights

The price of Zambia’s key staple crop, Maize, has seen a 45% increase year on year from May 2021 of $118 up to $215. This reflects a $2 drop in price from April 2022 ($217) reflecting reduced inflationary pressure on the commodity. The output for the 2021-22 season is estimated to be 2.7 million tons, 200 thousand tons below the national demand. It is estimated farmers can expect a decent profit at $180 – $250 per ton price range. The maize price is expected to increase by $230 as speculative buyers flood the market for cheap products for peak demand.

Soya is currently trading at $630 per ton, a 59% price increase from May 2021 ($260 per ton) and a 14% drop from April 2022 ($720 per ton). Global supply interruptions in Ukraine have caused the crop to skyrocket in price and the price sealing of $700 is reflective of supply shortage causing price pressure. Wheat closed it trading at $660 per ton, a 29% increase from May 2021 ($467 per ton) and a increase of 2% from April 2021 ($650 per ton). The wheat market has suffered significant disruptions as a result of the Ukraine war, prices at time of harvest are expected to be $550. Currently local production runs at 200,000 MT per year, 100,000 MT below the national demand (330,000 MT).

Key Economic Factors

Due to the ongoing war in Ukraine the price of commodities has increased by 33% from $800 per ton to $1200 per ton. The majority of supply is now dependent on the Chinese market due to bans of Russian chemicals, this in turn has resulted in significant supply chain issues. The price pressures reached their peak in March – April 2022 and is expected to reduce gradually as we reach harvest months (September – October 2022).

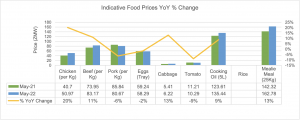

The general market trend is deflationary following the market trend of downward inflationary pressure. When assessing the indicative food survey, the data displays significant price falls in meat products from April – May 2022 including : Chicken (-6.85%, Beef (-0.75%) and Cabbage (-6.1%). However the YOY price changes reflect the increasing effects of global supply chain effects, with significant price rises in Chicken (+20% YOY), Beef (+11% YOY) and Mealie Meal (13% YOY).

Conclusion

Across the African markets the maize price fluctuated between $290 per ton (Tanzania) to between $313 – $335 per ton (Kenya), (Uganda). The prices peaked in Addis Ababa where Maize traded for $463 per ton and Wheat was trading for $820 per ton, $200 above the floor prices within the Zambian market. According to Chileshe Moono the Zambian market is in a disinflation cycle which is motivated by the pending IMF bailout package, estimated to be released in July. The monetary policy committee interest rate has been maintained at 9% and the Kwacha has been fluctuating between K17 – 20 per USD.

{kind=link}