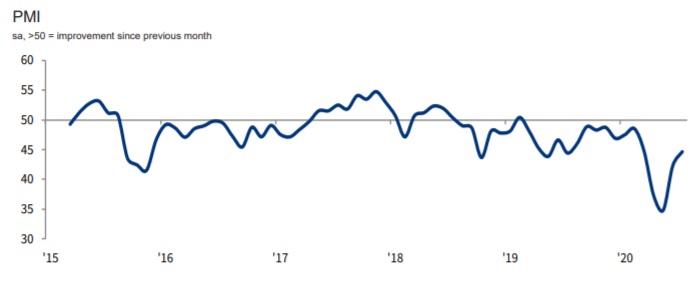

At face value, the latest Stanbic Bank Zambia Purchasing Managers Index, PMI, appears modestly encouraging. At 44.6 in July, the headline PMI was up from 42.3 in June and posted its highest reading since March and is much more ‘normal’ than the readings in the previous months. This may help rekindle the idea of a ‘V-shaped’ recovery, although, in reality, this is probably not what the data is telling us.

Of course, it is worth remembering that the index is still below the 50 level, which in normal times would indicate that output is falling, albeit at a much slower rate. The binary way in which the sentiment indices are formulated also potentially means the return to normality is being overstated.

PMI’s are constructed by asking private sector respondents whether they are seeing conditions improve or deteriorate – and unsurprisingly in July a much greater share of firms reported things getting better. The sectors covered by the survey include agriculture, mining, manufacturing, construction, wholesale, retail, and services. However, this improvement comes off a very low (in some cases, zero) base, and it also does not tell us anything about the magnitude of the rebound. We would, therefore, treat these figures with some caution, and in reality, think the size of the economy is still well down on its pre-virus size.

Business activity continued to fall in Zambia during July, according to the output index, extending the current sequence of decline to 17 months. Respondents generally linked the latest reduction in output to a lack of business due to the COVID-19 pandemic. The new orders index showed a lack of demand amid the COVID-19 pandemic and ongoing closure of some companies which led to a further reduction in new business in July. Challenges in securing new business meant that Zambian companies were able to keep on top of workloads in July according to the backlogs of work index.

In addition, the employment index showed that Zambian companies scaled back their staffing levels during July, extending the current sequence of job cuts to six months. The pace of reduction was sharp and faster than that seen in June. Respondents generally linked falling employment to a lack of sales. As has been the case in each of the past ten months, the quantity of purchases index indicates that companies recorded a drop in purchasing activity during July while the suppliers’ delivery times index outlined that Zambian companies reported a further lengthening of suppliers’ delivery times during the month, with the deterioration in vendor performance slightly stronger than that seen in June.

Anecdotal evidence suggested that delays in the receipt of imported goods were particularly prevalent as a result of border closures. There was a reluctance among companies to hold inventories amid pressures on cash flow and a lack of new orders. Stocks of purchases decreased for the tenth successive month, while overall input costs rose slightly in July, thereby ending a three-month sequence of decline. That said, the rate of inflation was weaker than the series average. Data suggested that the increase in overall input prices was reflective of higher purchase prices as staff costs decreased. Despite a rise in overall input costs, firms continued to lower their selling prices in an effort to attract customers.

Output charges decreased for the fourth month running while purchase costs increased for the first time in four months in the month of July, with respondents generally linking the rise to the weakness of the kwacha against the US dollar. With that also, the rate of inflation was only slight as demand for inputs softened. Staff costs decreased, and panelists linked this to a combination of lower workforce numbers, reductions in wages and cuts to working hours.

The future output index suggests that confidence among Zambian companies remained subdued at the start of this year’s third quarter. Although rising slightly, sentiment remained much weaker than the series average. Those respondents that predicted a rise in activity over the coming year expressed optimism that their businesses would be able to grow once the COVID-19 pandemic eased. On the other hand, the impact of the virus outbreak led some firms to remain pessimistic regarding the year-ahead outlook.

All in all, a continued reason for concern about the recovery is the expectation for employment in the months ahead. While service sector businesses are becoming more optimistic about demand, they are becoming more pessimistic about employment expectations in the months ahead thus continued monetary support is important. The current assumption is that the economy is not going through a V-shaped recovery and higher unemployment will only drag out the recovery phase.