Last week a tweet asking the ‘Zed Twitter’ community to explain bonds “like i’m 5” resulted in widespread conversation on government bonds led by financial educator Chanozya Kabaghe. As the demand for financial literacy coincides with an increase in incomes across the country, the appeal of making stable investments to secure the future for one’s family has become a priority. Bonds represent ownership of an instrument signifying a debt owed by a government or company for a fixed term with specific interest payments. Like bank loans, governments and institutions must pay interest on the bonds issued to members of the public and international. Unlike traditional debt which is paid in part over time, bonds are often paid in full at once in addition to interest earned over time. However, it is not as simple as it sounds, as investors often lose out on more lucrative industries and are locked into long term investments. In this article we explain bonds and give a summary of the current bond market in Zambia.

So What are Government Bonds ?

To explain bonds in the simplest terms, a bond is a financial instrument which serves as a form of raising funding for companies or countries through debt owed to large groups of individuals or companies. The bonds are ‘auctioned’ to individuals through banks and paid over a period ranging 10 – 20 years. So each bond you hold as an individual represents an obligation for a government (or company) to pay you the agreed interest as stated. Bonds can often be cheaper or less risky to operate than traditional bank loans and are often necessary when dealing with significantly large sums of money.

Ratings agencies such as Moodys, Standard & Poor and Fitch Ratings specialise in evaluating extensive factors which determine a country’s official credit score. This ranges from Aaa to D, with D signifying that a country is currently defaulting on its debt obligations. The rating each country or company receives determines the rate of interest charged on the bond, for example during COVID Zambia received a D for defaulting on a $29 million Eurobond payment in October 2020. We have since returned to CCC.

What is ‘Bond Maturity’

The term maturity represents the end of the bond period, at which point the original debtor is owed the ‘face value’ of the original debt which was purchased. For example you buy a 10 year bond at interest (coupon rate) of 10% annually at K1000. The payment that is due to the bondholder every year is calculated by dividing the total amount paid for bonds by this percentage number, in this case 10% of the original bond price = K100. Therefore the bondholder would receive K100 every year for 10 years totaling K1000 in interest payments. At the point of maturity the bond holder is then owed another bulk payment of K1000, for the ‘face value’ of the initial bond.

In some cases it can become complicated as some bonds lose value over time due to countries’ potential inability to pay. Zambian bonds for example are expected to mature at a rate of 56% of face value (external debt). What this means is that instead of getting the full value of your money back including interest you could risk losing money on ‘junk bonds’. While it rarely occurs that a country is unable to pay, often there is a risk of ‘debt forgiveness’ where bond holders must let go of the maturity payment having recouped profits in already paid interest. Zambian bondholders for example will earn 110% profit on their initial investment if our debt is not forgiven.

What is a ‘Bond Yield’

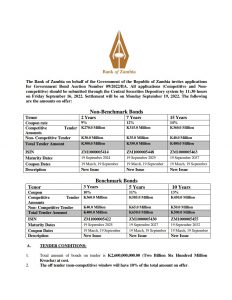

A bond yield is a number which determines how much money you receive in total after the bond has matured as a percentage of your original investment. This is calculated by adding the total of all annual interest payments + the original bond investment due once the bond matures. Currently Zambia’s international 10 year bond yields have a rate of 29%, meaning an investment of $1000 would result in payments totaling $3900. Please note this applies to the international market, our current rates stand at : 2 year – 9%, 7 year – 12% and 15 year – 14%. There is also a minimum investment of K1000 locally.

The bond yield is determined by something called a ‘Coupon Rate’. The coupon rate is the total amount of money you receive in payments each year / total value you paid for the bond. This determines the attractiveness of the bonds to resellers as the higher the coupon rate the higher the profit, but that likely comes with increased risk. The coupon date is the day on which the ‘coupon’ (interest) is paid either annually or bi-annually.

Benefits and Risks of using Bonds

By comparison, bonds tend to be less risky investments, especially with regards to developed and well established nations and businesses. There is also a thriving bond market globally which allows bondholders to sell their instruments for a profit. Individuals with significantly large sums of money which they may not need for their daily buisness can be stored away for the future and include interest payments to help maintain.

There is however a substantial risk that the business owner may lose out on substantial profits if they choose to invest in bonds over stocks. While more safe and sure, bonds traditionally provide significantly lower interest rates in return and tend to be ineffective if one is looking to increase their wealth. They are more accustomed to individuals who already have significant amounts of disposable cash.

How Do you buy them?

There are two methods two purchase bonds. The first and easiest is by visiting your banks treasury department and enquiring on opening the necessary accounts and paying the mandatory transaction fees. One can also approach the bank of Zambia directly with a valid recommendation letter from a bank to support.

{kind=link}