Access to credit in Zambia has become increasingly important as people seek out ways of getting money at a cheap cost. The biggest problem we have under or local credit markets is not that there isn’t enough money for everyone to access. Far from it. It is the plethora and complexity of credit options available.

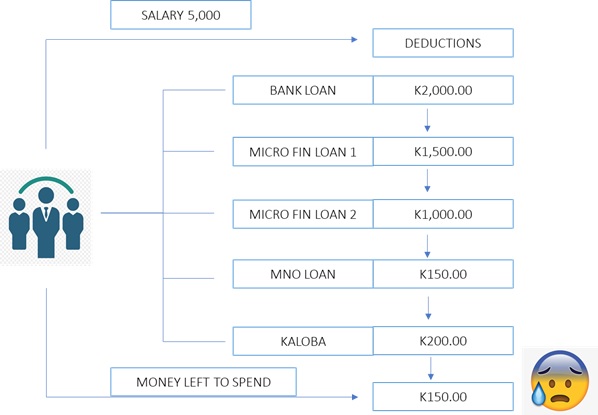

At present, a customer can access a Bank Loan, Microfinance Loan, Mobile Network Operator loan, and ‘Kaloba’ at the same time. These can be categorized is being formal and informal sources of credit. On the one hand, formal sources of credit are largely regulated with predictable terms and conditions, whereas on the other, informal sources of credit are based on unpredictable arm’s length agreements.

At present, a customer can access a Bank Loan, Microfinance Loan, Mobile Network Operator loan, and ‘Kaloba’ at the same time. These can be categorized is being formal and informal sources of credit. On the one hand, formal sources of credit are largely regulated with predictable terms and conditions, whereas on the other, informal sources of credit are based on unpredictable arm’s length agreements.

Although having a large number of credit options is a welcome situation, it does present a huge concern because people’s incomes have not been increasing at the pace of finance options despite access to credit is becoming easy. Furthermore, accelerating inflation has led to the weakening of consumer purchasing power whilst incomes remain in stagnation.

By being exposed to more options, a good number of such customers on numerous credit portfolios can easily give a raise in the number of non-performing loans especially during times, such as now, when there is an economic downturn.

The behavior shown above is becoming the “new normal” with customers which is now forming a significant amount of the credit portfolio in various businesses. This myriad of finance options creates a challenge in analyzing and determining the creditworthiness of a customer.

Data and consumer behavioral analysis can help in the segmentation of good from bad customers. Conventional credit reporting is done weekly or on a monthly basis but now with the introduction of Artificial Intelligence, credit reporting is now done in real-time with more efficient Credit scores.

Integrations with different APIs can also be used to provide insight into consumer behavior and trends. The soundness of a portfolio is no longer dependent on the number of customers a business has but identifying good consumer behavior and maintaining long term relationships.

In other words, it is better to have 20 customers with good credit scores and behavior compared to having 50 customers of whom 40 will give headaches while only 10 will be good performers.

A behavioral centric approach implies that the business can focus on providing excellent customer service and growth. This then leaves other parts of the business to focus on chasing customers on missed payments. In the end, taking advantage of technology can provide solutions to exiting credit management problems.